Can you fact-check the price of a prediction market bet?

Manipulation Matters Surprisingly Little

In 2024, prediction markets raised new questions about the meaning of a bet. When Fredi9999, an anonymous crypto trader on Polymarket, wagered millions on a Trump victory in the US Presidential election, the move shifted markets and stirred controversy. Predictably, Newsweek jumped in with a smear by association, labeling the market as “based offshore and partially funded by Peter Thiel”.

This jab at Polymarket has lost some bite in the days since the initial market movement. Now that prices have leveled across markets—including Kalshi, a US-regulated platform—new, more convoluted claims of potential “market manipulation” have sprouted up. With prediction markets going mainstream this year, it’s time to step back and break down the basics of how market mechanics operate. Because anybody crying manipulation ought to understand how things are supposed to work.

Is it manipulation or is it liquidity management?

Isaac King explains in “Prediction Markets Are Not Polls” how buying shares of an outcome, like “Rocket yes” or “Rocket no”, directly influences the prices in the market. In this play example, the “Rocket yes” buyer either has enough capital or is operating in a market with such low liquidity that each purchase moves the price, starting from 50 cents, and inching upward as the market reacts. This happens because market makers adjust prices based on supply and demand.

For example, let's say the question is "Will NASA's next rocket launch successfully?", and by default the market starts at 50%. I can buy a share of YES for 50 cents, and it's worth a whole $1 if the rocket does in fact launch; I can double my money! But if the rocket doesn't launch, then my YES share is worth nothing at all, and I lose my investment. The best financial decision is to only buy shares if they're cheaper than the expected value of those shares.

That is, if I know that out of all rockets NASA has ever launched, 95% of them have launched successfully, and nothing is different about this one, then that means each YES share is worth 95 cents to me. If I can buy them for only 50 cents, that's free money! For every YES share I buy, the market probability goes up slightly, so maybe the second share I have to pay 51 cents for, then the next share I have to pay 52 cents, etc. Eventually the market price reaches 95 cents, and now it's no longer in my favor to keep buying.

Market makers are middlemen who make it unnecessary for buyers and sellers to find each other directly. They adjust prices in real-time, smoothing out sharp swings from big or poorly timed orders by providing liquidity. The extent of this “manipulation” can be measured in the spread, or the difference between the buy and sell prices of a “Rocket yes” share. By comparing these spreads across different markets operating the same bets, we can quantitatively assess how efficiently each market operates.

Is it manipulation or is it trading fees?

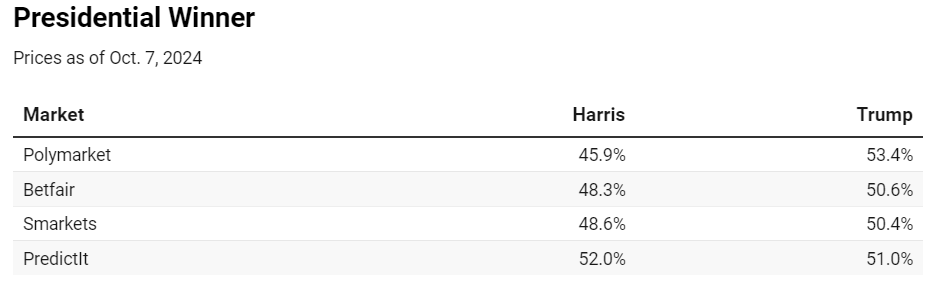

In “Margin of Inefficiency in Prediction Markets”, Harry Crane measures some other inputs to the price of a bet that have less to do with the underlying probability of the event, and more to do with the operating costs of running the market itself. After all, different markets charge different trading fees and commissions. Using this “Margin of Inefficiency”, Crane is able to make an apples-to-apples comparison for odds on the same event (specifically, Trump vs Kamala) between different markets on Oct 7:

A first glance at these tell very different stories, with Donald Trump the favorite at Polymarket, Betfair, and Smarkets, and Harris the favorite on PredictIt. However, once the margin of inefficiency of these markets is factored in, we see that all markets are, technically, consistent with a narrow range of true probability values.

[…]

Therefore, applying the concept of margin of inefficiency, we could conclude that the consensus market forecast for Harris as of October 7 is between 46.27% - 47.23% and, conversely, the market consensus forecast for Trump is between 52.07% - 52.73%. (The market consensus forecast is defined as the range of probabilities that is consistent across all markets after accounting for margin of inefficiency.)

PredictIt’s prices are heavily adjusted due to the high fees associated with trading on the platform. For example, if a contract is priced at $0.50 and the true probability of the event is 53%, you’d expect a profit of $0.03 in a perfectly efficient market. But with PredictIt’s 10% commission on profits, that turns into a $0.02 loss after fees. A 5% withdrawal fee further widens the margin of inefficiency, meaning a contract priced at $0.50 reflects a true probability of somewhere between 40.25-59.75%.

Is it manipulation or is it information asymmetry?

What looks like manipulation is often just information asymmetry—the inequality of who knows what, and when. As Robin Hanson explains in Shall We Vote on Values, But Bet on Beliefs?, speculative markets excel at quickly aggregating the best information from the most informed traders. Compared to other institutions “on the same topics, with similar resources”, markets allow those with more accurate data to exert a greater influence on outcomes:

The main robust and consistent finding is that it is usually quite hard, though not impossible, to find info not yet incorporated in speculative market prices. [xvi] In laboratory experiments, speculative markets usually aggregate info well, even with four ignorant traders trading $4 over four minutes. [xvii]

[…]

In addition to lab studies, a few studies directly compare real speculative markets with other real info institutions. For example, racetrack market odds improve on the prediction of racetrack experts [xxii]; orange juice commodity futures improve on government weather forecasts [xxiii]; stocks fingered the guilty firm in the Challenger crash long before the official NASA panel [xxiv]; Oscar markets beat columnist forecasts [xxv]; gas demand markets beat gas demand experts [xxvi]; betting markets beat Hewlett Packard official printer sale forecasts [xxvii]; and betting markets beat Eli Lily official drug trial forecasts. [xxviii]

The largest known tests compare bet prices to major opinion polls on US presidential elections. For example, in 709 out of 964 comparisons, bet prices were closer to the final result. [xxix] This gain comes in part from prices being disproportionately influenced by active traders, who suffer less from cognitive biases. [xxx]

Hanson points out a few exceptions to how well speculative markets aggregate information. The clearest example is the financial bubble, where inflated prices are only obvious after the fact. Bubbles stick around because betting against them is risky, and price corrections take too long for specialists to bother. Still, even during the dotcom and housing bubbles, speculative markets flagged over-investment more reliably than most so-called experts. This superior accuracy comes from incentives.

Traders with skin in the game work harder to eliminate their own biases. Manipulators, who trade based on factors other than asset value, may distort prices in the short term, but in doing so, they create opportunities for more informed traders to trade against them. In fact, speculative markets with more of this “noise trading” or manipulation attempts, tend to be the most accurate in the long run.

Ultimately, what many label as “manipulation” is just market mechanics doing what they do best—aggregating information, correcting distortions from noise, and sharpening the bets of informed traders. So if you think the price is wrong, don’t just complain—trade against it and prove the market wrong. After all, in prediction markets, it’s not about who you are, but what you know.